The Finances of Buying and Renovating a $35,000 Home in Detroit

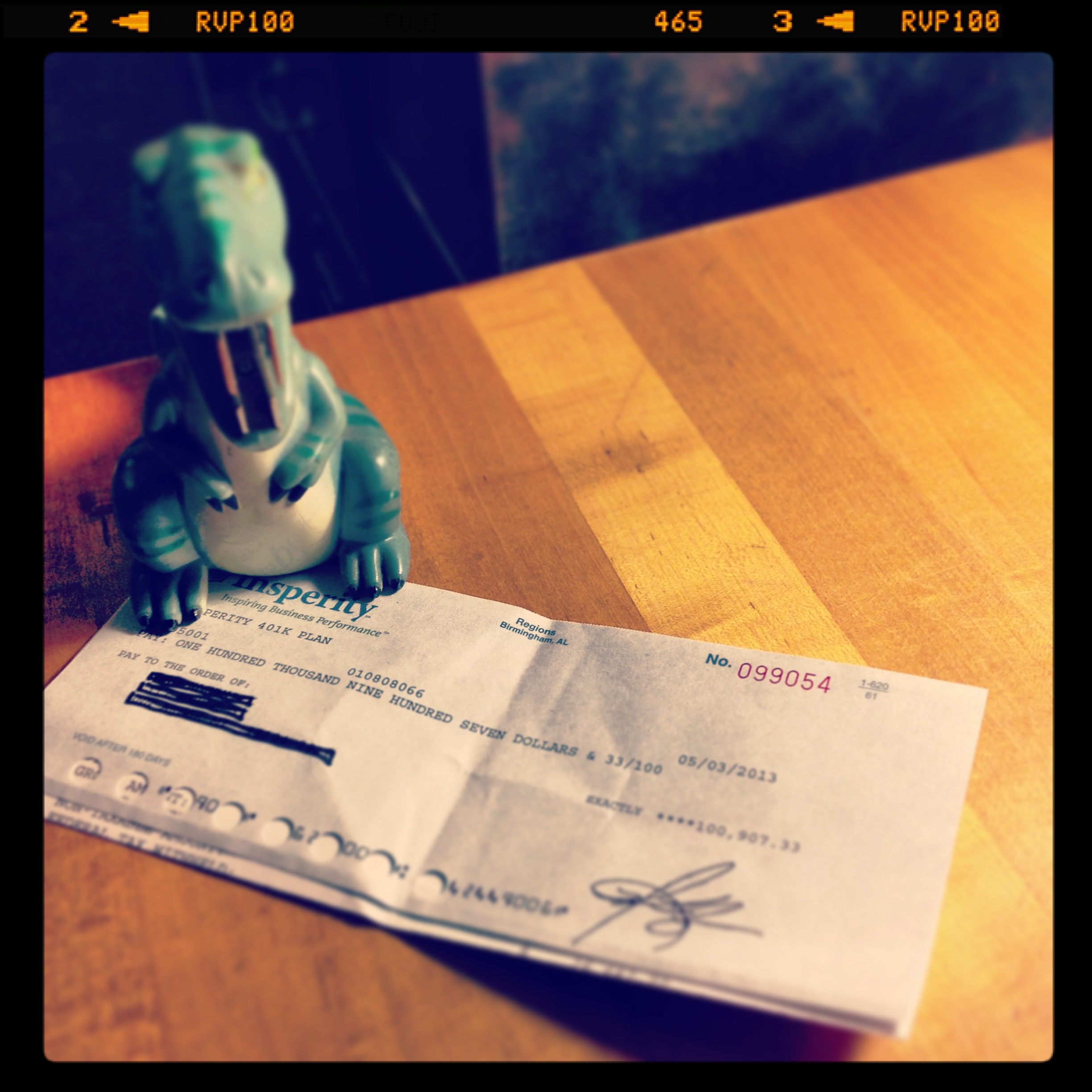

That’s what a $100,000 check looks like. Don’t expect to ever have that on my desk again.

When we say that we are cashing out our life savings to restore this house, it’s a bit of hyperbole, but not by much. So let me explain what exactly it means.

To make this project happen, we had to have cash. Detroit is a cash kind of town. Cash makes things happen.

Properties under $50,000 can’t even get a mortgage, and the median home price in the city hovers around $10,000. Most of those properties need *a lot* of renovation, but it’s hard to find a bank that wants to lend you money to fix up a house that’s worth less than $50,000. It’s a chicken-and-the-egg problem.

We might have been able to scrape together the $35,000 purchase price creatively. (Hello, cash withdrawl from credit cards!) But that wouldn’t have given us enough for the renovations. So we decided to cash out Karl’s 401(k) — the one he’s been diligently saving in for the past 13 years. Plus we’ll take some additional cash from our IRAs.

What do these finances look like exactly? Well, here’s the math. (I’ve been a personal finance editor, and I’ve asked families to really open their books to me. So in honor of that, I’m going to be pretty transparent about the money here on our blog.)

Life savings:

- Karl 401(k): $133,000 +

- My IRA: $43,000 +

- Karl IRA: $35,000 =

Total life savings: $211,000

Just looking at these numbers makes me feel rich. Uncomfortable. Privileged.

I come from poverty, not retirement savings. My mother is working for peanuts at JC Penny’s. My family has been known to bring in road kill so that the animal’s life isn’t wasted and there’s meat in the freezer. I’ve had to pawn things just to get through to payday. The cycle of credit card debt? Oh, yeah.

But when I look at our balance sheet, I realize how lucky I’ve been. I went to college – the first in my family – and had the opportunity to get a good job with a good paycheck and good benefits. My parents couldn’t imagine what my life would look like, but they sacrificed to make sure it would involve something more stable than theirs. And it put me in a place to meet and marry Karl. And most of our security is directly related to Karl’s careful ways. He’s frugal in every area except beer.

What I’m saying is that we’re lucky. We don’t have trust funds or family money as our safety net, but we have enough to take a risk.

And it’s a big risk. What we have in our life savings matches up exactly with what we need to complete the project (we think):

Cost to buy and renovate the house:

- Purchase: $35,000 +

- Closing costs: $1,000 +

- Renovations: $175,000 =

Total cost of the house $211,000

UPDATE: $211,000….. hahahahahaha. Yeah, right.

The first real estimates just came in. We go cry now.

Unfortunately, due to taxes and penalties for breaking into one’s life savings before age 59½, we don’t actually have $211,000. Any time you crack these savings plans, you need to knock at least 30% off the top for the IRS. That leaves us roughly $50,000 short of our goal.

So, here’s what we are doing:

1. We cashed out the $133,000 401(k).

After taxes, that left us with about $101,000. Of course, don’t forget, this isn’t free money. We still must pay the 10% IRS penalty for an early withdrawal. So we’ll have at least another $13,000 tax hit come April 2014. Plus, depending on where this puts in terms of tax brackets, we could owe more income tax.

It was helpful, for me, to think of the taxes this way: I’m going to pay them one way or another. Because a 401(k) deals in pre-tax dollars, you save now without paying taxes. But that means you pay them when you start making withdrawals after 59½. (Note: we are talking about 401(k)s; the rules are slightly different for traditional and Roth IRAs.) But regardless, I have to fork over the money at some point, and I need it now for a major purchase that will hopefully leave me owning a home free and clear. (Tax accountants would be horrified; you usually pay less tax in retirement than you do breaking into you money at the height of your earning power.)

2. We are each taking $10,000 out of our IRAs.

You can take up to $10,000 per spouse out of your IRAs without getting hit with another 10% by the IRS if you use the money for a primary home purchase. This is a once-in-a-lifetime offer; you can’t do it every time you go to buy a house. So while we’ll have to pay the taxes on this money (lalalalalalala pretend this isn’t happening), at least we don’t have to pay the penalty. This gives us another $20,000.

So where does that leave us:

- Cash in the bank: $121,000 ($101,000 + $20,000)

- Cash remaining in retirement savings: $58,000 (give or take the taxes)

Gap between the costs and our available cash: -$53,000

For now, we’re going to try very hard to leave that $58,000 in our retirement savings. That’s our “in case of emergency, break glass” money. We want the power of compounding interest to still be working it’s magic on something. Yes, I realize this is probably ridiculous considering the fact that we just cashed in a $133,000 account. (We all have our quirks.) But, since I come from nothing, I actually really l like the idea of leaving a little bit protected. It makes me feel like there is a small safety net in case we get into trouble.

So how are we making up the gap? Funny you should ask. Um, we’re not entirely certain.

First, we’re going to live on one salary. Once Karl has a job we will be saving all of his paychecks. Since we’ll be doing part of the renovations in stages, projects will have to wait until we’ve saved. This is going to take a long time.

Another option is to take out a loan once the first phase of the project is completed. The house will appraise for more than it will now (real estate prices in Detroit are on the rise!), and we can show that we’ve put a significant amount of our own capital into the project. So that’s a possibility, but I really l like the idea of getting out of all this with no mortgage payment and very little debt.

What kind of loan, though, is still a question. An FHA renovation loan? A construction loan? A home equity loan? A cash-out refi? This, my friends, is called foreshadowing to future posts on this very blog.

Finally, hope for a rich benefactor to take pity on us. A long shot, but worth hoping for.

And that, my friends, is what a gamble looks like. I hope my poker skillz are strong.

6 Responses to “The Finances of Buying and Renovating a $35,000 Home in Detroit”

I will keep my eyes peeled for rich benefactors to send your way. After skimming a little off the top myself, possibly.

How’s 10% sound? 🙂

Go for the long odds and the big pay-off Lotto Ticket! ie. only buy the one with the winning number

Stacy and I have an annual subscription to the New York lotto 🙂

Keep in mind: capitoal gains on primary residence are not subject to ANY tax.

Look into a 203K loan right away. You can get them retroactively within the first 6 months you own. We couldn’t do it because (1) we aren’t employed in Michigan; and (2) we weren’t ready with all of our reno drawings and contractors, etc., within six months. (If you don’t make the window, you can reapply after a year of ownership.)

Just remember that appraisals are the chicken-egg problem in The D. Until houses start selling at above construction cost, it’s hard to get enough moola to cover what it costs for re-construction of a house. The house plans (with two floors complete) appraised at $145K. Community Reinvestment Act lenders (e.g., those with 203K programs and others) can sometimes do better than “market” value.

If you are considering using your finances to start you and a loan to finish you off, you might quickly explore doing the reverse. If you have the backhoe gassed up and ready to go, this will put a delay on the construction while you do all the paperwork. But if you don’t have the funds to get you all the way there, it may worth considering.

Call Southwest Lending for starters. I can get you at least one other name.